Systematic investing has been well established in the equities space for decades now. It has attracted academic interest, millions of dollars of investments, and the proliferation of a wide range of investment products.

Fixed income has been different. When I recently implemented a major shift in my own portfolio, I discovered a wide range of systematic equity products that even retail investors can choose from, and yet on the fixed income side, hardly anything was available or easily accessible. The question is why?

I think there are two reasons. First, data availability has been a long-standing problem. While single stock market data going back to the 1920s has been relatively easily accessible for decades, data availability on the fixed income side, particularly in credit, has been nowhere near that rich. Second, for a long period of time, fixed income markets have lacked the level of development and availability of trading instruments that allows the implementation of systematic strategies.

Things are changing now. Fixed income data production is shifting from investment banks to data vendors, making it far richer and more easily accessible than ever before. Academia, where most of the systematic approaches in the equity space were developed, is picking up research efforts on systematic fixed income approaches[1]. Meanwhile, fixed income markets continue to grow and in most credit segments already offer a level of development that enables the usage of sophisticated and dynamic investment strategies. As Ben Dor et. al (2021) write in their excellent book Systematic Investing in Credit – “scientific credit investing stands today where scientific equity investing stood at the turn of the century: in an uncrowded space and on the threshold of considerable secular growth”[2].

The aim of this article is to provide an overview of what systematic fixed income investing is and to explain why I find this approach highly appealing and promising.

What is systematic fixed income and is it any different from fundamental investing?

Systematic (also known as rules-based/algorithmic/quantitative) fixed income management is a data-driven investment approach that relies on statistically significant and repeatable dependencies.

A common misconception about systematic investment strategies is that they are black boxes with little to no visibility of what the algorithm is doing. While this may be true for some newer Artificial Intelligence-driven approaches which rely on data mining, it is certainly not the case with systematic investment strategies. What these strategies do is applying the scientific method in practice.

As anyone with an undergraduate degree knows, the scientific method starts with an idea of why a certain phenomenon exists. This idea is then used to form a hypothesis, which itself is subsequently tested and potentially rejected using statistical methods and tools.

What is crucial to repeat is that the scientific process starts with an idea, not with data. And, importantly, that idea may very well represent a fundamental principle such as, for instance, the notion that relatively cheap assets tend to outperform relatively expensive ones. Therefore, it is perfectly valid to claim that fundamental and systematic/quantitative investing are effectively the same, and the only difference between them is the tools used to apply the same basic principles in practice.

Still not convinced? Let me offer you a research paper that I found surprising too. In a study from 2019, Brooks, Tsuji, and Villalon analyzed the track record of four legendary investors – Buffet (Berkshire Hathaway), Soros (Quantum Fund), Lynch (Fidelity’s Magellan Fund), and Gross (PIMCO’s Total Return Fund). The article is listed in the reference section below in case you are interested in reading it yourself.

I am sure no one in their right mind would consider these investors quants, and yet the paper provides evidence that most if not all of the alpha they generated can be explained by a handful of systematic style factors. By no means does any of the findings in this paper degrade the extraordinary work of these people; it merely shows that these exceptional investors intuitively understood the power of systematically applying a specific investment approach and, even more importantly, sticking with it through thick and thin (which itself is extraordinarily difficult and deserves huge appreciation in its own right).

All of that brings me to the reason why I am such a fan of systematic investing. A well-designed systematic strategy is transparent as it is based on fundamental factors rooted in behavioral biases and/or market inefficiencies. It can be backtested and easily discarded if it doesn’t meet objective statistical criteria. A well-designed systematic strategy is predictable and reliable (in statistical sense) and is most certainly not a “secret sauce” that no investor can ever understand.

What types of systematic fixed income strategies exist?

Before going any further, it is important to clarify what type of systematic fixed income strategies exist. Some systematic strategies offer exposure to specific risk premia – both traditional and alternative ones, while others capitalize on index or market inefficiencies. Let’s take a closer look.

Providing exposure to alternative risk premia

Value, Momentum, Carry, and Quality – some of the multitude of style factors known in the equity space – are also applicable in the world of fixed income investments. Here are the fundamental ideas that lay behind these factors:

- Value – the idea that relatively cheap assets tend to outperform relatively expensive ones

- Momentum – the concept that assets that have outperformed in the recent past will continue to do so in the near future

- Carry – the notion that higher-yielding assets tend to outperform lower-yielding ones

- Quality – the idea that high quality and low-risk assets tend to outperform (on a risk-adjusted basis) low quality and high-risk assets

Although still small in its footprint, there is a growing body of research showing that these alternative risk premia/style factors are also prevalent in the fixed income space[3]. In a 2018 study, Brooks, Palhares, and Richardson (Brooks et. al., 2018) test the validity of style factors on global government and U.S. corporate bond data[4]. The study demonstrates important and compelling findings. First, there is evidence that correlations between individual style factors are low to negative, ranging between 0.5 and -0.4[5]. Second, the study shows that style factors exhibit low correlation to traditional risk premia such as credit risk, bond term risk, and equity risk premium[6], suggesting significant diversification benefits to traditional long-only fixed income credit portfolios. Third, there is evidence of “very little sensitivity…to various macroeconomic state variables that are typically a concern for investors (e.g. shocks to inflation, shocks to economic growth, shocks to real yields, shocks to liquidity, and shocks to volatility) and meaningfully less sensitivity to these variables than the underlying asset classes” (Brooks et. al., 2018, page 3) . In simple words, because these style factors/alternative risk premia are rooted in behavioral biases and/or market inefficiencies, their ability to deliver positive returns is not conditional on any specific economic environment.

Are these results universal? Are they observable and exploitable in less efficient markets or do they remain confined to the most developed and liquid segments of the credit fixed income market?

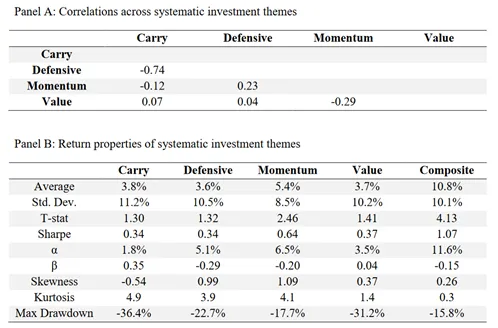

In 2020, Jordan Brooks, Scott Richardson, and Zhikai Xu (Brooks et. al, 2020) attempted to answer these questions by investigating the applicability of systematic investment approaches within the space of my beloved Emerging Markets debt. One critique I have on this study is that it only focuses on EM hard currency debt, leaving out EM local debt – a real pity in my view given how fast this market segment currently grows. Nevertheless, the study still delivers some highly compelling results. Similar to what is observed in developed credit markets, the paper provides evidence that style factors such as carry, defensive, momentum, and valuation “are well compensated and lowly correlated in EM markets” (Brooks et. al, 2020). Furthermore, the study demonstrates that the correlations between these style factors/systematic risk premia are even lower in the EM space than in DM credit, meaning that combining them into a single portfolio produces a return stream with a slightly positive skew – a feature I find particularly impressive given how negatively skewed Emerging Markets debt as an asset class is[7] .

Figure 1: Style risk premia in the EM debt space – correlations (Panel A) and return characteristics (Panel B). Notice the slightly positive skew that the combined portfolio (labeled Composite in Panel B) exhibits.

There will be a whole series of articles on this website covering the ins and outs of style factors. But the silver lining across both published and my own research is that style factors can provide substantial diversification benefits to traditional long-only fixed income portfolios.

Capitalizing on market inefficiencies

Because only a small proportion of bond investors act in a truly unconstrained manner, while the majority of them face regulatory and/or investment policy-related restrictions, certain repeatable market phenomena occur, which represent attractive opportunities for systematic strategies to exploit. As with style factors, I will go deeper in this topic in a separate series of articles, but here is a short teaser of how these systematic strategies can deliver value-add.

Fallen Angels is a well-known term for bonds that experience a downgrade from Investment Grade (IG) to High Yield (HY). There is a large group of institutional investors which for regulatory and/or internal investment policy reasons are restricted to holding IG bonds only. When IG bonds get downgraded to HY and become Fallen Angels, IG-only investors are forced to divest their holdings within a relatively short period of time. This creates significant selling pressure which cannot be compensated by the natural demand from dedicated HY-investors[8]. As a result, Fallen Angels experience an excessive drop in prices as their spreads widen far above what would be considered fair values. Or at least that is what the theory suggests.

The question is – do Fallen Angels really suffer from such mispricings and if they do, by how much? Is this phenomenon observable with all Fallen Angels or is there some differentiation among them? How long does it take for Fallen Angels’ spreads to peak and (as the selling pressure gradually dissipates) how long does it take for spreads to normalize and tighten back to “fair-value”-levels?

Answering these questions is important because it can be the key to a potentially attractive investment strategy, which in its simplest form would look like this: observe which bonds are downgraded from IG to HY, wait for the forced selling from IG-only investors to dissipate, differentiate among the most mispriced/attractive ones, buy those bonds, and enjoy handsome outperformance as spread levels gradually normalize.

Ben Dor et. al. (2021) provide extensive research on the viability of this strategy[9]. I am not going to cover their interesting findings in detail here (this will come in later articles) but here is a short summary. On a relative basis (i.e. compared to risk-matched HY peers) it takes 6 months on average for Fallen Angels’ spreads to peak. As the selling pressure eases off, Fallen Angels (again, on average) tend to enter a process of spread normalization which continues up to 24 months after the original downgrade from IG to HY. Yes, there are significant discrepancies between individual Fallen Angels, creating the need to establish a robust and objective screening and selection process. And yes, one can construct a viable strategy that capitalizes on Fallen Angels’ mispricings and produces attractive uncorrelated alpha with a net-of-costs Information Ratio of 0.5 to 0.6[10].

Capitalizing on index inefficiencies / characteristics

While some researchers tend to combine market and index inefficiencies into one bucket, I view them as separate phenomena that can be exploited individually by systematic fixed income strategies.

Because the fixed income management business is predominantly benchmark-oriented, index inefficiencies will continue to impact the return profile of most fixed income investors. Indices are in effect systematic constructs – they are rules-based and thus predictable, which in turn allows for the construction of systematic strategies that exploit these weaknesses.

More specifically, a scientific approach can be applied to optimizing areas such as new issuance dynamics, new inclusion dynamics, issuer concessions, and other index characteristics with a potentially significant impact on portfolio performance. Addressing these areas is important because benchmark-oriented fixed income investing comes with a number of performance drags related to transaction costs, taxes, and others. Reducing or eliminating these drags by applying systematic approaches in the context of benchmark-oriented fixed income portfolios can be the key to producing persistent uncorrelated alpha, and I plan to provide more details on these approaches in future articles on this website.

Performance Implications of Portfolio Characteristics[11]

The last area where systematic fixed income investing has a useful application is the research of how bond and portfolio characteristics impact performance.

Take coupons for example. It is common knowledge that coupons impact the price and duration of a bond. Two bonds from the same issuer with the same maturity but different coupons would have different duration and prices (higher coupon = lower duration and higher price). If I asked you, however, whether coupons had a relationship to spread levels/credit risk, what would you say?

Or consider something much more topical – ESG scores. Do portfolios with higher ESG scores outperform portfolios with lower ones? Or does the increased demand in bonds with high ESG scores inflate their prices and erode any advantage brought by the reduction of risk for negative credit events?

Fortunately, there is a growing body of research that attempts to answer these questions, and we are going to dive deep into it in the future.

What benefits does systematic fixed income offer in the context of broader fixed income allocation?

A systematic investment strategy is not perfect because after all, it can only be as good as the human who designed it. Designing good systematic strategies is not easy as it requires extensive knowledge and experience, especially when it comes to a multidimensional, complex, and relatively illiquid asset class like for example fixed income credit.

What can’t be denied though is that rules-based investment strategies remove the human component from the day-to-day decision-making process, which in stressful situations may be detrimental to performance due to emotions and/or behavioral biases. To this point, here is a quote from Robert Carver, former head of fixed income at AHL, from his book Systematic Trading describing some of his experiences during the Global Financial Crisis of 2008-09: “Our computer system had stuck to its preprogrammed set of trading rules and mechanically exploited the marker moves almost to perfection, whilst terrified humans had discussed closing it down” (Carver, 2015, p. 3).

The second crucial benefit of systematic strategies, and here I am specifically referring to fixed income ones, is their potential to be a powerful diversifier in the context of traditional portfolios. As noted in the previous section, systematic strategies offer access to alternative risk premia which are neither highly correlated with the traditional fixed income risk factors nor with economic environment variables. Thus, systematic strategies are capable of materially improving not only the Sharpe Ratios but also the return profile (as measured by skew, maximum drawdown, etc) of investors’ overall allocation to fixed income.

Are systematic and discretionary active fixed income management approaches incompatible?

To be clear, I am not arguing against active fixed income managers. Having worked for such a manager for almost 8 years, it would be hypocritical for me to state that.

I do believe, however, that there is a place for systematic fixed income strategies within every investor’s portfolio for all the reasons I outlined in the previous section.

I also believe that discretionary active managers can benefit from the introduction of systematic components to their investment process. Yes, market phenomena such as the Fallen Angels price dynamic I described above are known in the active management investment community. The same goes for most of the index inefficiencies I mentioned. However, as long as a discretionary active manager’s approach to capitalizing on these inefficiencies is not systematized and optimized in a robust fashion, I see plenty of room to improve their investment process by introducing a systematic tilt to it.

Conclusion and investment implications

Like anything else in life, I think the question of whether or not systematic fixed income strategies have a place in traditional fixed income portfolios doesn’t have a simple yes or no answer. On the contrary, I think that investors can make their fixed income portfolios significantly better if they manage to skillfully blend exposures to both discretionary and fully systematic fixed income managers. As for discretionary active managers – I think they can benefit as well from systematizing segments of their investment process, especially when it comes to utilizing market and index inefficiencies.

For all these reasons I am very excited about the future of quantitative/systematic fixed income strategies and I believe they are bound to gain traction and popularity among the investment community.

If you are equally excited and share my interest in systematic/quant fixed income strategies, do please connect by leaving a comment below or using the contact form on this website. Also, let me know if you have any preference for which topic I should cover next.

Thanks and looking forward to connecting with you!

Sign up to get articles like this straight

into your inbox.

By subscribing you agree to receive emails from systematicbonds.com and agree with the Website’s

Privacy Policy. You may unsubscribe at any time.

References

Ambastha, M., Ben Dor, A., Dynkin, L., Hyman, J. and Konstantinovsky, V., 2010. Empirical Duration of Corporate Bonds and Credit Market Segmentation. The Journal of Fixed Income, p.5-27.

Ben Dor, A., Desclée, A., Dynkin, L., Hyman, J. and Polbennikov, S., 2021. Systematic investing in credit. Hoboken, New Jersey: John Wiley & Sons, Inc.

Brooks, J., Moskowitz, T.J., 2017. Yield Curve Risk Premia., Working paper, AQR,.

Brooks, J., Palhares, D. and Richardson, S., 2018. Style Investing in Fixed Income. The Journal of Portfolio Management, 44(4), pp.127-139.

Brooks, J., Richardson, S. and Xu, Z., 2020. (Systematic) Investing in Emerging Market Debt. SSRN Electronic Journal,.

Brooks, J., Tsuji, S. and Villalon, D., 2019. Superstar Investors. The Journal of Investing, 28(1), pp.124-135.

Carver, R., 2015. Systematic trading. Hapmshire, Great Britain: Harriman House Ltd.

Houweling, P. and van Zundert, J., 2017. Factor Investing in the Corporate Bond Market. Financial Analysts Journal, 73(2), pp.100-115.

Israel, R., Palhares, D. and Richardson, S., 2018. Common Factors in Corporate Bond Returns. Journal Of Investment Management, 16(2), pp.17-46.

Notes

[1] To illustrate this point, just consider typing “systematic fixed income” in Google Scholar and you will discover that over 50% of all search results are papers written in 2021 (data as of January 2022). Granted, the number of results is relatively small but what is important is the trend, not the absolute numbers.

[2] Ben Dor et al. 2021, page xv

[3] A selection of the limited number of papers include Brooks and Moskowitz (2017), Houweling and van Zundert (2017), and Israel et al. (2018).

[4] The study uses JPM Government Bond Index as a proxy for the global government bond investment universe. For the US corporate bond universe, the study uses BAML US Corporate Master Index (Investment Grade) and BAML US High Yield Master Index (High Yield).

[5] See Exhibit 3, Brooks et al. (2018)

[6] See Exhibit 4, Brooks et al. (2018)

[7] For the period January 2000 – December 2021, the Bloomberg Barclays USD Aggregate Total Return Index (BBG Ticker: EMUSTRUU) has a realized skew of -2.22 based on monthly total return data. SOURCE: Own calculations, Bloomberg

[8] This is comment is made by Ben Dor et al (2021), page 82 and is based on a previous study from Ambastha et al (2010) which documents a high level of segmentation in credit markets between IG and HY-only investors. , Ben Dor, Dynkin, Hyman, and Konstaninovsky (2010). Intuitively, the mismatch between IG-only sellers of Fallen Angels and HY-only buyers also makes when considering the mismatch in sizes between the IG and HY segments of the corporate bond market, which is approximately 8 to 1 (data as of December 2015, Source: Bloombegr Barclays, AQR, London Business School)

[9] In fact, the dedicate whole 3 chapters of their book “Systematic Investing in Credit” to Fallen Angels systematic strategies

[10] Ben Dor et. al (2021) construct a portfolio of Fallen Angels which they measured against a risk-matched HY benchmark . In different specifications, their models achieve an Information Ratio of 0.48 to 0.64. See Ben Dor et. al. (2021), p. 116.

[11] I am borrowing this title from the Systematic Investing in Credit by Ben Dor et. al. (2021)

disclaimer

The information in this article is for personal, non-commercial use only. All content of this article is for general informational purposes only. No information included in this article is investment advice of any kind. Plamen Todorov (“The Provider”) is a publisher and not an investment advisor. The Provider does not make any investment recommendations, nor does the Provider intend to influence users of this article in their personal investment decisions. None of the ideas in this article are meant to be construed as professional and / or financial advice. Readers of this article are solely responsible for their investment decisions. In exchange for using this Website and reading this article, you agree not to hold the Provider or any third party service provider which is connected to this website liable for any possible claim for damages arising from any decision you make based on information or material made available to you through this website.

© 2022 Systematic Bonds. All rights reserved. Plamen Todorov holds the international copyright to all content on this website. Any usage of text or images from this website is permitted only with the prior written consent of Plamen Todorov.